Home

Market

STOCK PICK: Transformers & Rectifiers India (TAR...

Market

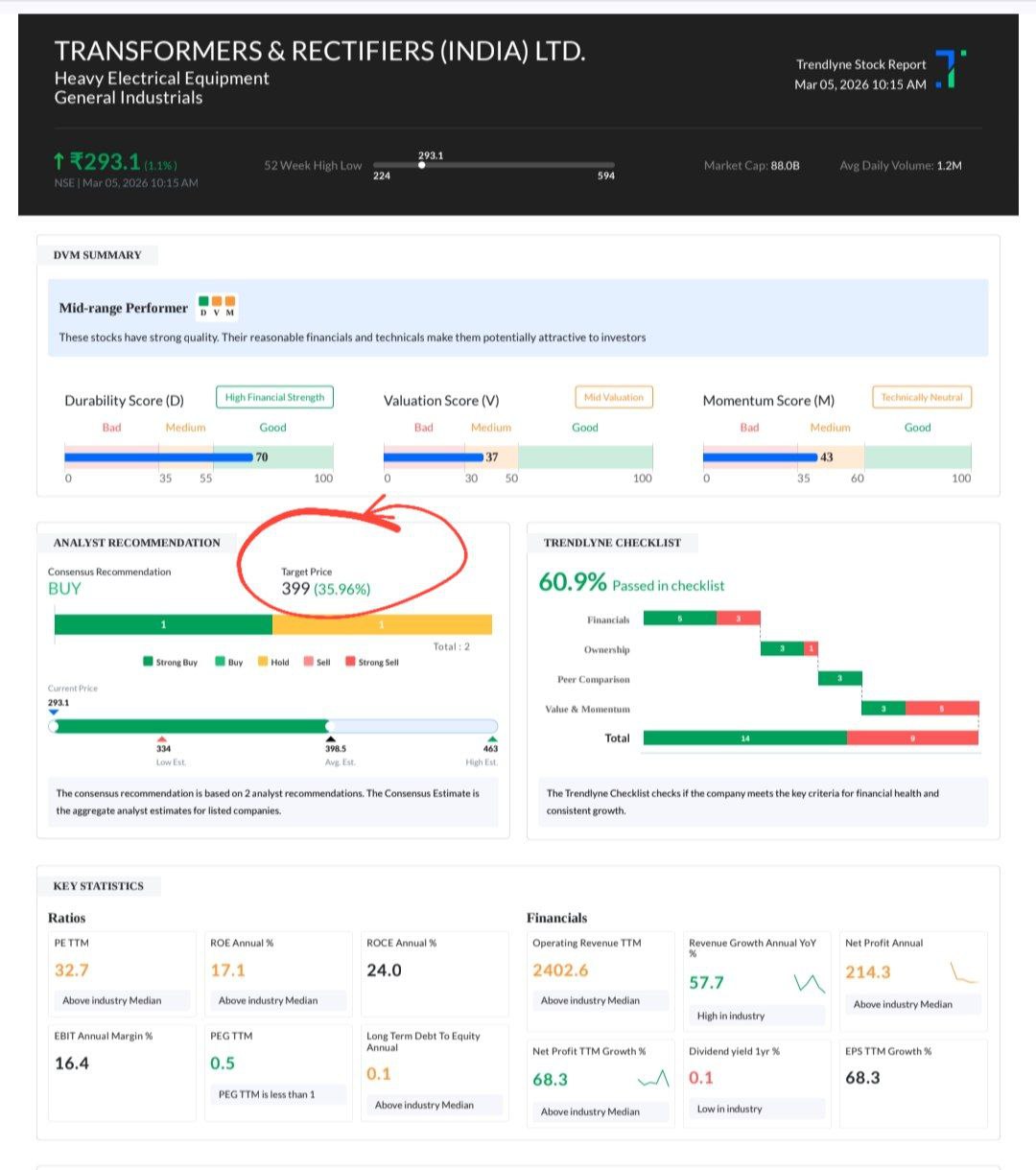

STOCK PICK: Transformers & Rectifiers India (TARIL) — Analysts See 36% Upside to ₹399, Ventura Capital Bets on ₹700 Target

Civic Watch Media | Truth. Accountability. Public Interest.

March 5, 2026 | Investment Analysis — Mumbai