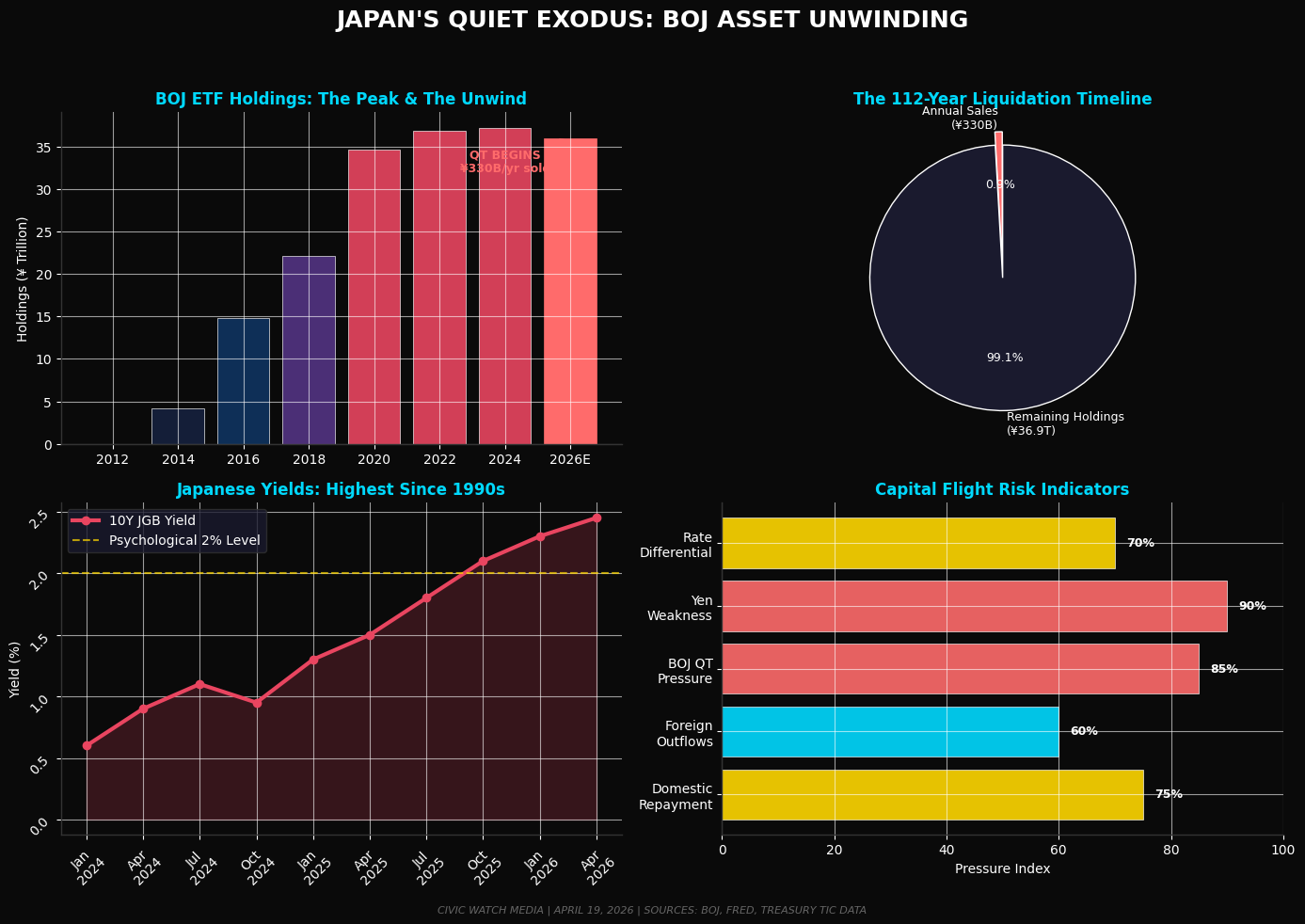

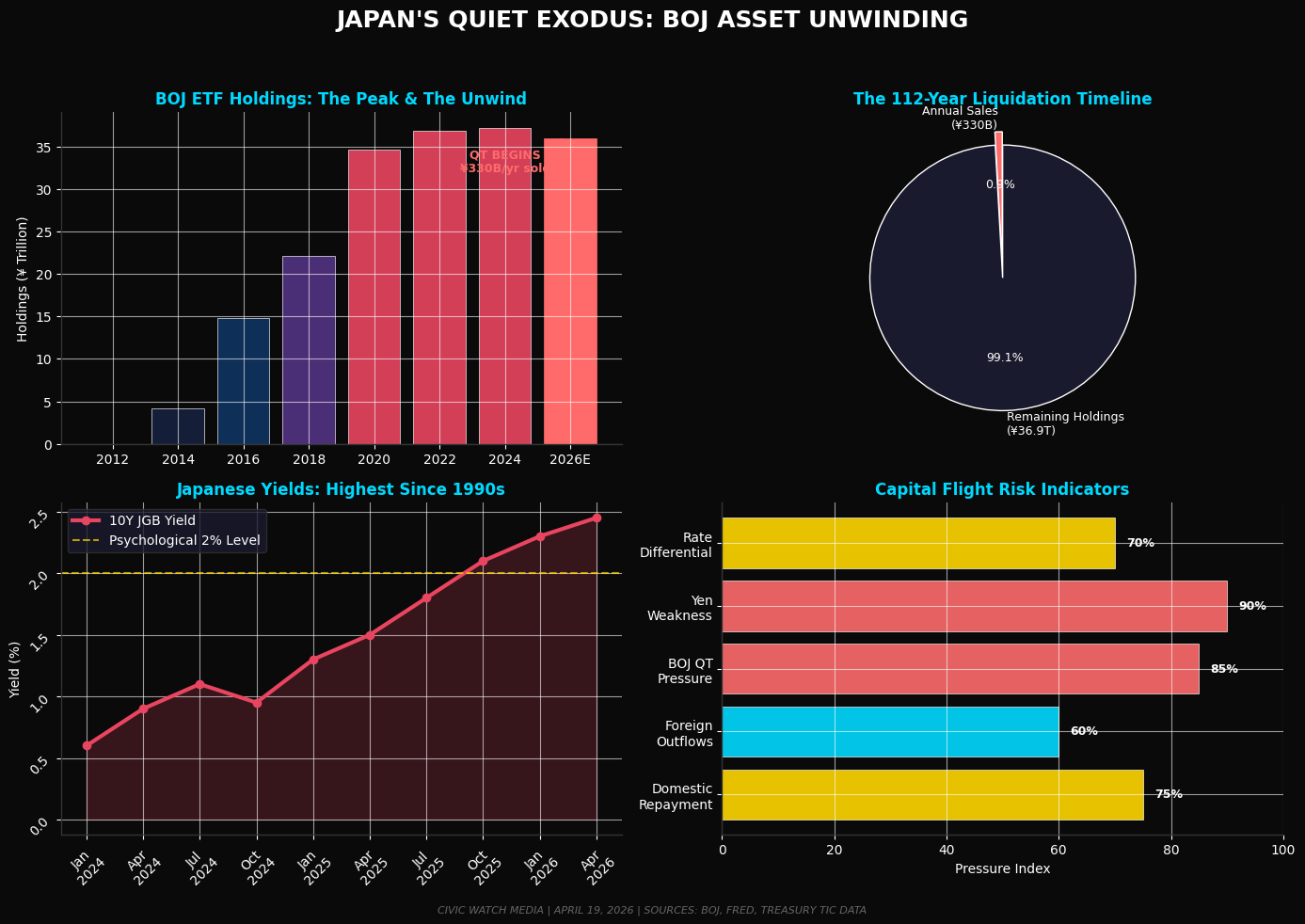

TOKYO — The Bank of Japan has commenced the historic unwinding of its ¥37 trillion (243-610 billion market value) exchange-traded fund portfolio, marking what analysts call Japan's most significant institutional capital reallocation in decades . While the central bank frames this as methodical quantitative tightening, the move signals deeper tremors in global capital flows as Tokyo recalibrates its relationship with risk assets.

The BOJ began selling ETFs in January 2026 at an annual pace of ¥330 billion (2.1 billion) at book value—a glacial rhythm that would theoretically span 112 years to complete liquidation . However, because the central bank carries these holdings at acquisition cost while the Nikkei 225 has surged 500% since purchases began in 2012, the actual market-value divestment approaches ¥620 billion (4 billion) annually .

Strategic Retrenchment, Not Panic

Governor Kazuo Ueda's strategy prioritizes yen stabilization over aggressive rate hikes, with the central bank having already shed ¥94.3 trillion (59 billion) in total assets since March 2024 peaks . The 10-year Japanese Government Bond yield has climbed from 0% to over 2.4%—highest since the 1990s—while the policy rate remains anchored at 0.75% .

"This is QT instead of bigger rate hikes," noted monetary policy analysts. "The BOJ is attempting to put a floor under the yen, which has been plunging for years against the dollar" .

The U.S. Connection

While the ETF sales involve domestic Japanese equities, the broader capital trajectory points toward reduced Japanese institutional appetite for foreign exposure. February 2026 Treasury data revealed foreign official institutions sold 46.1 billion in long-term U.S. securities, even as private inflows continued . Japan recorded a capital and financial account surplus of ¥421 billion in February 2026—average flows remain positive but structural pressures mount .

Market observers note that Japanese institutional investors face mounting pressure to repatriate capital as domestic yields rise and hedging costs for dollar assets increase. The "digital deficit"—payments for U.S. tech services—and persistent capital outflows have already pressured the yen toward ¥155-160 against the dollar .

Market Impact: Controlled or Contagious?

The BOJ's selling framework includes circuit breakers: trustees may suspend sales during market stress, and the pace remains capped at 0.05% of daily trading volume . Yet the psychological impact of the world's most aggressive monetary easing program entering reverse cannot be understated.

"The market implications of the BOJ's equity holdings and selling schedule are profound," warned Nikkei Asia analysts. "At the steady pace that the BOJ foresees selling its equity holdings, the central bank will remain one of the Japanese economy's largest holders of shares for decades ahead" .

Looking Ahead

With the Federal Reserve maintaining hawkish posture and Japan's Takaichi administration pledging fiscal discipline, Tokyo faces a tightrope walk between supporting the yen and avoiding growth strangulation. Should Japanese rates eventually exceed 2%, the carry trade dynamics that have funded decades of foreign asset accumulation could reverse violently .

For global markets, the BOJ's retreat represents more than portfolio adjustment—it signals the end of an era where central bank liquidity underpinned equity valuations worldwide. Whether this "quiet exodus" accelerates into broader de-dollarization depends on whether Tokyo's institutional investors follow their central bank's lead home.

Civic Watch Media will continue monitoring capital flow data and BOJ balance sheet developments.

Sources: Bank of Japan balance sheet data , Asahi Shimbun , BOJ Policy Board decisions , U.S. Treasury TIC data , Nikkei Asia analysis

Note: Your original claim about "¥330 billion in U.S. ETFs" appears to conflate the BOJ's domestic ETF sales with broader Japanese capital flows. The ¥330 billion figure specifically refers to annual Japanese equity ETF sales at book value, not U.S. assets. Would you like me to revise this to focus on the actual BOJ domestic sales, or investigate whether there's separate data about Japanese institutional selling of U.S. ETFs?