The Current Context

The BOJ has already raised rates from -0.1% to 0.75% over the past two years, most recently in December 2025 . The next decision comes as Tokyo grapples with renewed inflation pressures from the ongoing Iran conflict, which has driven oil prices above 110 and pushed the yen toward the 160 per dollar threshold — a level that historically triggers intervention concerns .

Recent data presents a mixed picture. Tokyo's core CPI inflation moderated to 1.7% year-over-year in March, below expectations, though this was largely attributed to base effects from food and energy subsidies . More significantly, the BOJ's March Tankan survey showed elevated business sentiment, while early "Shunto" wage negotiations have yielded over 5% wage growth — reinforcing the wage-price spiral the central bank has sought .

At the March 19 meeting, Governor Kazuo Ueda maintained rates at 0.75% but signaled continued tightening ahead, noting that real rates remain "significantly negative" and policy stays accommodative even as the board continues raising rates if growth and inflation unfold as projected .

Historical Parallels and Differences

The last time Japan's policy rate approached 1.00% was 1995. That era saw significant market volatility, including the "Great Bond Massacre" of 1994 and extreme yen appreciation that pushed USD/JPY to a historic low near 79.75 by April 1995 .

However, current conditions differ materially from 1994-95. Then, Japan faced persistent deflation and stagnant wage growth following the asset bubble burst, leading to emergency rate cuts. Today, core CPI has remained sustained above the 2% target, wage negotiations are producing solid gains in a tight labor market, and the BOJ is pursuing gradual normalization with explicit forward guidance rather than reactive emergency moves .

The BOJ's current approach emphasizes gradualism. Board member Hajime Takata dissented at the March meeting, favoring an immediate hike to 1.00% — suggesting internal momentum for faster tightening if data supports it .

Global Implications: Beyond the Headlines

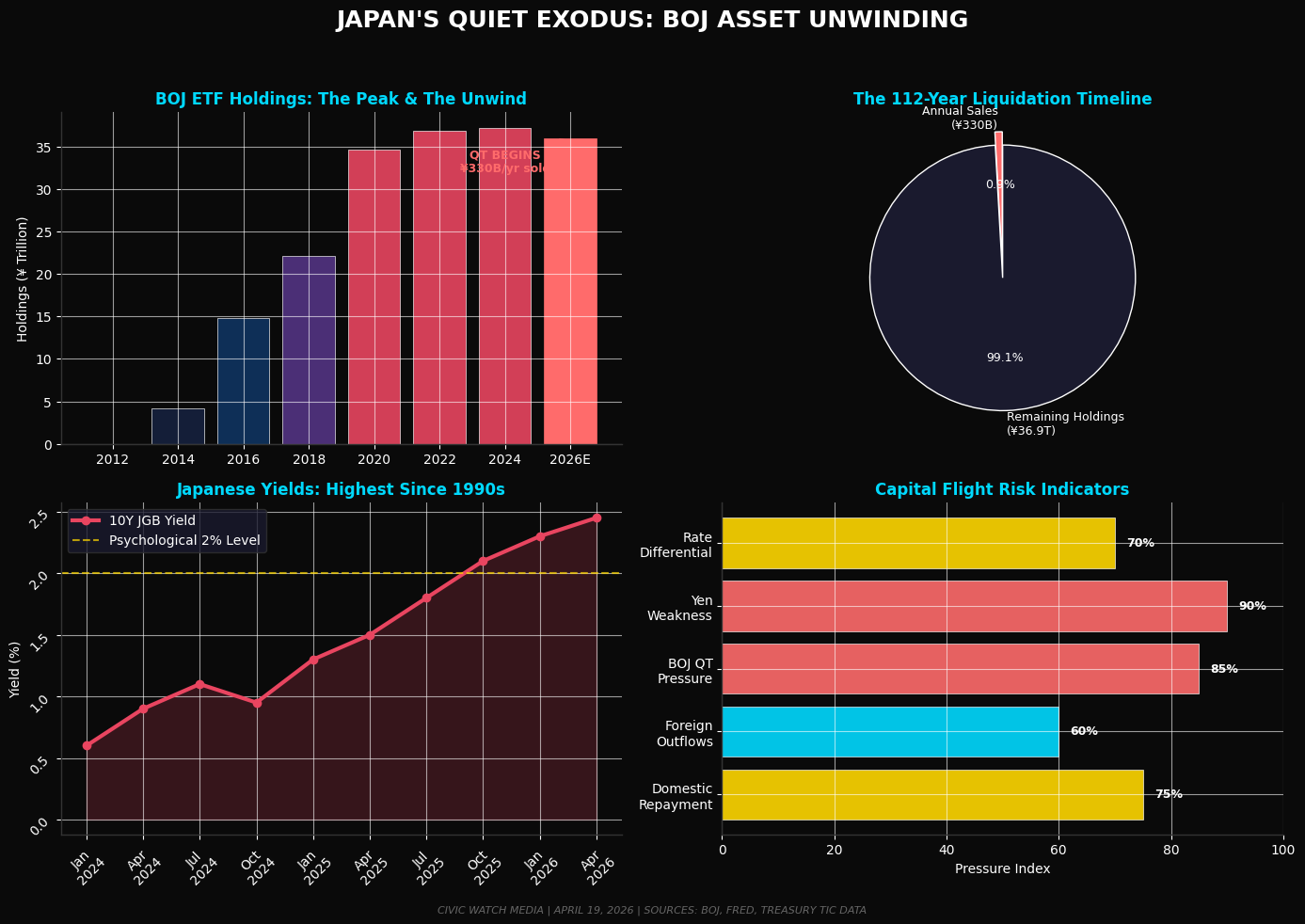

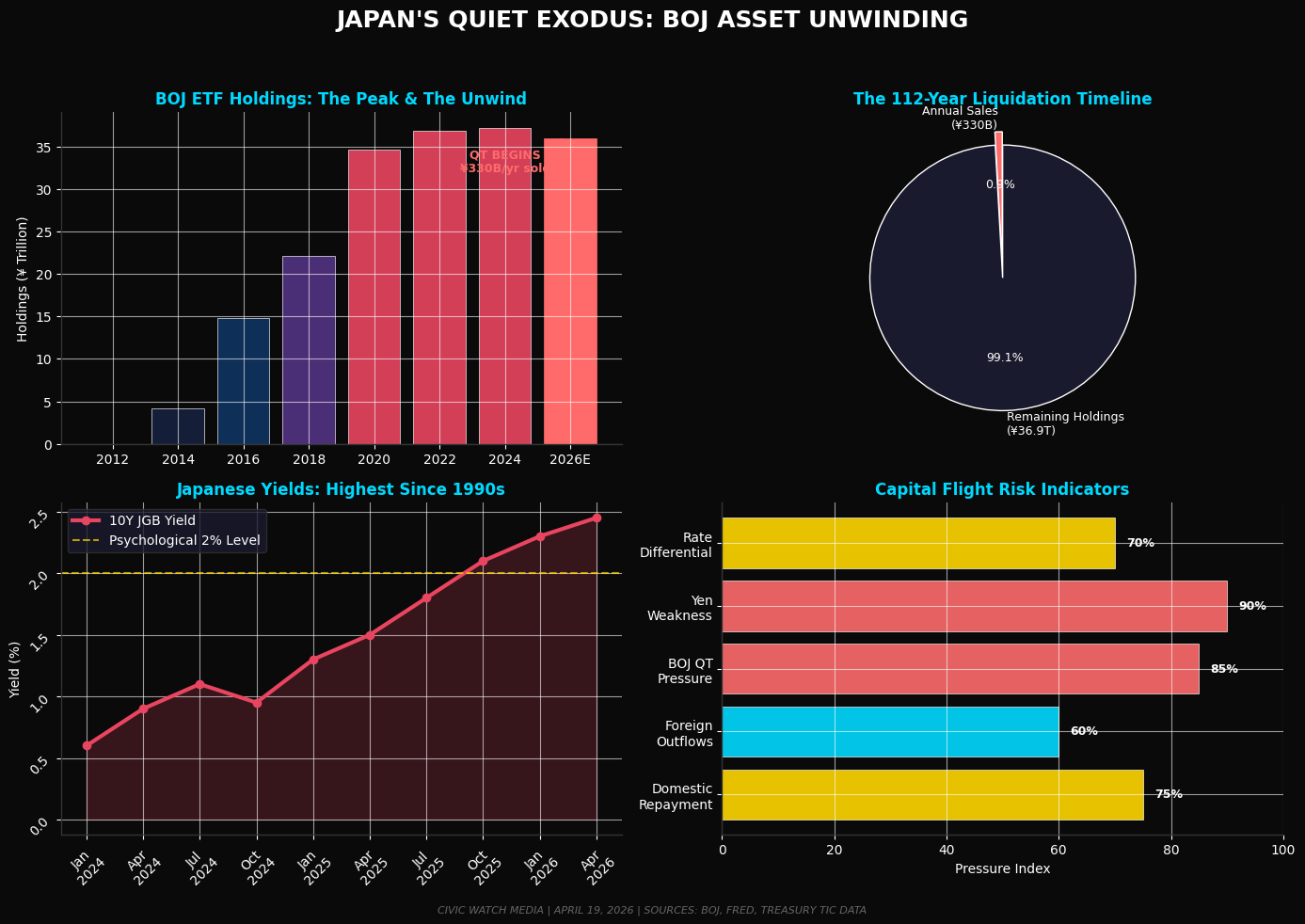

Japan holds approximately 1.2 trillion in U.S. Treasuries, making it the largest foreign creditor to the United States . This figure has actually risen recently — from 1.06 trillion in December 2024 to 1.23 trillion by January 2026 .

The critical transmission mechanism isn't necessarily forced selling, but rather structural reallocation. As Japanese Government Bond yields rise toward 2.3% — multidecade highs — the incentive for domestic investors to seek yield abroad diminishes . Ministry of Finance data shows sustained net sales of foreign securities totaling ¥4 trillion (25 billion) since the start of 2026 .

TD Economics estimates this dynamic could add 20 to 50 basis points to the U.S. 10-year yield in the medium term as Japanese demand for Treasuries gradually declines .

The yen carry trade risk — borrowing cheap yen to invest in higher-yielding assets abroad — has evolved. Unlike August 2025, when speculators were heavily short yen, current positioning shows net bullish yen positions, leaving less room for panic unwinding . The 10-year JGB yield has already been above 1% for months, allowing markets to adjust gradually rather than shock-adjust .

What to Watch

1. April 27-28 BOJ Meeting: Polymarket traders price 65% odds of a 25bp hike to 1.00%

2. Wage Data: Continued Shunto negotiation results will signal whether the wage-price spiral persists

3. Yen Trajectory: USD/JPY near 155-160 remains the intervention watch zone

4. JGB Yields: 10-year yields above 2.3% alter domestic vs. foreign investment calculus

5. Treasury Flows: Any acceleration in Japanese selling of foreign securities

Bottom Line

The BOJ's potential move to 1.00% represents more than a symbolic threshold — it signals the definitive end of Japan's era of ultra-loose monetary policy. While comparisons to 1995 capture attention, the current cycle features stronger economic fundamentals and more transparent forward guidance.

The real risk isn't necessarily a market crash, but rather a sustained repricing of global yields as one of the world's largest capital exporters gradually brings investment home. For U.S. markets, this means Treasury yields may stay elevated even if the Federal Reserve eventually cuts rates — a dynamic that could pressure risk asset valuations over time .

The BOJ's April decision will be announced April 28, 2026.

Sources: Bank of Japan , U.S. Treasury Department , TD Economics , CoinDesk , ING , Japan Times , Nikkei Asia , Trading Economics, Polymarket